Rates - Details and Examples

In This Topic...

The rating system in the Bridge Specialty Suite is a powerful and versatile structure that enables extremely complex calculations to be performed. This section provides detailed descriptions of how the rates features function and interact.

See the Rates section for instructions on adding rates to a master cover.

Premium Type

The final value of each premium type is used to calculate all other related values, such as taxes and commissions.

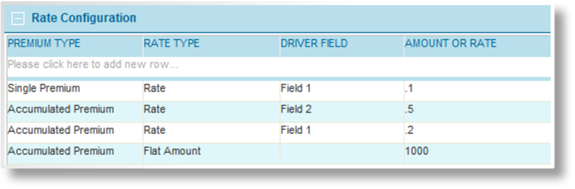

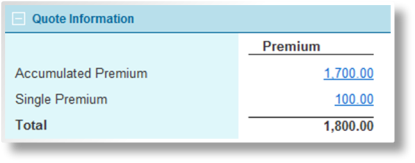

Example: The following Rate Configuration table includes two premium types. The Single Premium has one result, calculated as 10% of Field 1. The Accumulated Premium is the total of three results, 50% of Field 2, 20% of Field 1, and a flat amount of 1000.

If the submission has 1000 entered into both Field 1 and Field 2, the quoted premiums are as follows:

|

Accumulated Premium: |

1000 x 0.5 = 500 1000 x 0.2 = 200 1000 1700 |

|

Single Premium: |

1000 x 0.1 = 100 |

Rate Type

The rate type defines what calculation, if any, is performed for each entry in the Rate Configuration table. All calculations for the same premium type and sequence number are performed in a specific order (see Sequence below). Each calculation is performed on the accumulated value of all preceding calculations for the same premium type and sequence number.

Rate

A Rate is calculated by multiplying the value of the Driver Field in the submission form by the value of the Amount or Rate field. The result is added to the accumulated value.

The Amount or Rate field is commonly a decimal value representing a percentage, such as 0.1 to represent 10%. However, any positive number can be used.

Examples:

If the Driver Field equals 1000 and the Amount or Rate is 0.5 (50%), the calculated value would be 500.

If the Driver Field equals 5000 and the Amount or Rate is 0.02 (2%), the calculated value would be 100.

Multiplier

A Multiplier is calculated by taking the accumulated value and multiplying it by the value of the Amount or Rate field. The result becomes the new accumulated value.

The Amount or Rate field can be any positive number. Values over 1 result in an increase, and values between 0 and 1 result in a decrease.

A Driver Field is not required. If one is specified, the value of the driver field is multiplied by the Amount or Rate value and the result is multiplied by the accumulated value.

Examples:

If the accumulated value is 4000, and a Multiplier of 1.5 is applied, the new value of the Premium Type is 6000.

If the accumulated value is 5000, and a Multiplier of 0.2 is applied, the new value of the Premium Type is 1000.

If the accumulated value is 1000, a Driver Field has been selected and has a current value of 200, and a Multiplier of 3 is applied, the new value of the Premium Type is 600,000 (1000 x 200 x 3).

Notes:

Since all values are multiplied by each other, a zero value anywhere in the multiplier results in a final zero value for the accumulated value at this point in the calculations. If the driver field is left blank, it is considered a 1, having no effect on the calculation.

While the Multiplier functionality may appear similar to Discount or Surcharge, the behavior is different in two ways:

- More than one Multiplier calculations are compounded, with each multiplier being applied individually. More than one Discount or Surcharge calculations are combined before being applied. See the Sequence section below for details and examples.

- The calculated result of a Multiplier becomes the new accumulated value. The calculated result of a Discount or Surcharge is added to or subtracted from the accumulated value.

Flat Amount

As the most direct type of rate, the Flat Amount adds or deducts the Amount or Rate from the accumulated value.

The Amount or Rate field can be any number. Positive values are added to the accumulated value, and negative values are deducted. The Driver Field is not used.

Examples:

If the accumulated value is 4000, and a Flat Amount of 2000 is applied, the new value is 6000.

If the accumulated value is 5000, and a Flat Amount of -2000 is applied, the new value is 3000.

If the accumulated value is 0, and a Flat Amount of -2000 is applied, the new value is -2000.

Tip: Deducting a Flat Amount could result in a negative value. To prevent this, a Minimum rate type of 0 can be applied immediately after the Flat Amount calculation. See the Sequence section below for information on controlling the order of the calculations.

Minimum

The accumulated value is compared to the value of the Amount or Rate field. If the total is less than the Amount or Rate field, it is increased to that amount.

The Amount or Rate field can be any positive number.

Examples:

If the current value of the Premium Type is 4000, and a Minimum of 5000 is defined, the new value of the Premium Type is 5000.

If the current value of the Premium Type is 4000, and a Minimum of 3000 is defined, the Premium Type is not changed.

Discount or Surcharge

A Discount or Surcharge is calculated by taking the accumulated value and multiplying it by adjusted versions of the Amount or Rate field or Driver Field. The results are added to or subtracted from the accumulated value.

The Amount or Rate field can be any positive number. Values over 1 result in a surcharge, and values between 0 and 1 result in a discount. A value of exactly 1 has no effect.

A Driver Field is not required. If one is specified, the value is used as a second Amount or Rate, calculated against the accumulated value and then added or subtracted at the same time as the value calculated from the Amount or Rate. To use the Driver Field value instead of the Amount or Rate, enter 1 in the Amount or Rate field.

Since the Amount or Rate value and the Driver Field value each perform the same calculations from different source values, it is most common to use one source or the other, but not both.

Important: The values used in the Amount or Rate field and Driver Field represent the intended result of the calculation. 1.5 equals a 50% surcharge, while 0.5 equals a 50% discount. However, the provided values are adjusted by -1 in order to isolate the actual amount of the discount or surcharge. When multiple discounts and surcharges are applied at the same time, this prevents the original accumulated value from being multiplied.

Examples:

If the accumulated value is 4000, and a Discount or Surcharge of 1.5 is applied (a 50% surcharge), the new value of the Premium Type is 6000.

1.5 - 1 = +0.5 (the isolated surcharge rate)

4000 x +0.5 = +2000 (the actual surcharge)

4000 + 2000 = 6000

If the accumulated value is 5000, and a Discount or Surcharge of 0.2 is applied (an 80% discount), the new value of the Premium Type is 1000.

0.2 - 1 = -0.8 (the isolated discount rate)

5000 x -0.8 = -4000 (the actual discount)

5000 - 4000 = 1000

If the accumulated value is 1000, a Driver Field has been selected and has a current value of 1.8 (an 80% surcharge), and an Amount or Rate of 0.6 is applied (a 40% discount), the two values are calculated and applied separately against the current accumulated value.

1.8 - 1 = +0.8 (the isolated surcharge rate)

1000 x +0.8 = +800 (the actual surcharge)

0.6 - 1 = -0.4 (the isolated discount rate)

1000 x -0.4 = -400 (the actual discount)

The new accumulated value is 1400 (1000 + 800 - 400).

Notes:

A value of 0 in either the Amount or Rate field or the Driver Field results in a 100% discount. A value of 1 should be entered to represent no discount or surcharge. If no Driver Field is selected or the Driver Field is blank, it is not included in the calculations.

The Discount or Surcharge type does not work with premium grids.

While the Discount or Surcharge functionality may appear similar to Multiplier, the behavior is different in two ways:

- More than one Multiplier calculations are compounded, with each multiplier being applied individually. More than one Discount or Surcharge calculations are combined before being applied. See the Sequence section below for details and examples.

- The calculated result of a Multiplier becomes the new accumulated value. The calculated result of a Discount or Surcharge is added to or subtracted from the accumulated value.

Driver Field

The Driver Field column is used to select a field from the workflow to be used for the calculations of certain rate types. The selected field may be a value entered directly by the user, or may be a calculated field that generates a value based on several options throughout the workflow.

Amount or Rate

The Amount or Rate field contains the value to be applied according to the rate type. See the individual Rate Type descriptions for details on what values are permitted.

The Attachment and Limit fields can be used together or separately to define what portion of the Driver Field value should be used for the calculations in the selected entry. If neither field is used, the full value is used for calculations.

Attachment

When used without a Limit entry, only the amount of the Driver Field that exceeds the Attachment value is used for calculations. Essentially, the Attachment value is deducted from the Driver Field value (with a minimum value of 0) and the result is used for the calculations. This does not change the actual Driver Field value.

The Attachment field can be any positive number.

Examples:

If the Driver Field equals 4000, and an Attachment value of 1000 is defined, the calculations are performed using a Driver Field value of 3000.

If the Driver Field equals 2000, and an Attachment value of 3000 is defined, the Driver Field is considered 0 and is not used in the calculations. For Multiplier and Discount or Surcharge rate types, the calculations are still performed on any accumulated total of the Premium Type.

Limit

When used without an Attachment entry, this defines the maximum amount to be used from the Driver Field. If the Driver Field value is less than or equal to the Limit value, the full Driver Field value is used for the calculations. If the Driver Field value exceeds the Limit value, the Limit value is used for the calculations. This does not change the actual Driver Field value.

The Limit field can be any positive number.

Examples:

If the Driver Field equals 4000, and a Limit value of 3000 is defined, the calculations are performed using a Driver Field value of 3000.

If the Driver Field equals 2000, and a Limit value of 3000 is defined, the calculations are performed using a Driver Field value of 2000.

Attachment and Limit

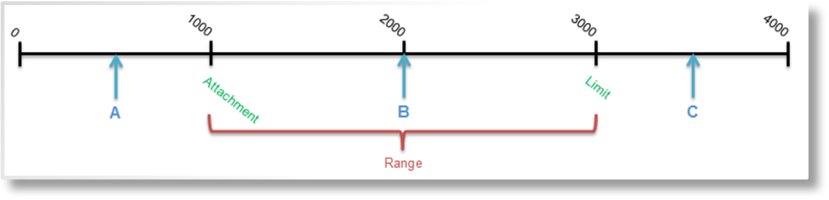

When used together, Attachment and Limit values define a range of the Driver Field to be used for the calculations, sometimes known as Rate Layers. The Attachment value defines the beginning of the range, and the Limit value defines the end of the range. Only the portion of the Driver Field value that falls within that range is used.

Examples:

In the chart above, the Attachment value is set at 1000 and the Limit value is set at 3000. This defines the Range of the value that can be used for calculations.

If the Driver Field equals 500, shown as Point A in the chart, it is considered 0 since it is less than the Attachment value.

If the Driver Field equals 2000, shown as Point B in the chart, 1000 of that value falls within the range. That 1000 is used for the calculations.

If the Driver Field equals 3500, shown as Point C in the chart, 2000 of that value falls within the range. That 2000 is used for the calculations.

Trigger Name

A trigger can be defined to control if an individual entry is applied or not. If the trigger does not evaluate as true, the entry is skipped and the system proceeds to the next entry in sequence.

Sequence

While many premiums have fairly simple calculations, some formulas can include several factors that must be processed in a specific order, or contain calculations that should only be applied to certain values and not the entire premium type. Sequence numbers can be used to isolate calculations from each other.

Calculations start with the that has the lowest initial sequence number, and all entries for that premium type are completed in order of sequence. The system then proceeds to the premium type with the next-lowest initial sequence number. If any rate calculations are to be based on the calculated results of another premium type, the initial sequence numbers should be kept unique to ensure the proper order of the calculations.

For each premium type, the system works through the calculations starting with entries without sequence numbers, followed by sequenced entries from the lowest value to the highest. All entries within the same sequence number are processed in order (see below), with the results of each calculation being passed to the next calculation within the same sequence number. Once all sequence numbers for a premium type have been completed, the accumulated values from all sequence numbers are added together to create the final gross premium amount for that premium type.

For each , all entries with the same sequence number (including no sequence number) are handled according to Rate Type in the following order:

- Rate

- Flat Amount

- Discount or Surcharge

- Multiplier

- Minimum

All entries with the same Premium Type, Sequence number, and Rate Type are handled as follows:

|

Rate |

Each rate is calculated separately and added to the accumulated value. |

|

Flat Amount |

Each amount is added to the accumulated value. |

|

Discount or Surcharge |

Multiple entries are combined to determine a total discount or total surcharge, which is then applied to the accumulated value. |

|

Multiplier |

Each multiplier is applied separately. |

|

Minimum |

Only one minimum should be applied for a single sequence number. |

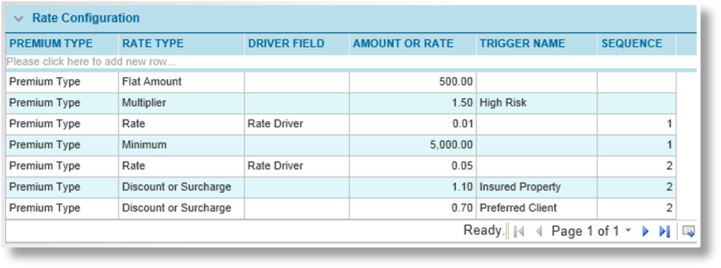

Example: The sample scenario below presents a calculation that requires careful sequencing. This example does not use unique sequence numbers, in order to illustrate how the default order of Rate Types can affect the sequence.

(unneeded columns have been hidden)

- A Flat Amount is added for administrative fees. With no Sequence number, and flat amounts being the second Rate Type to be processed, this is the first calculation.

- A Multiplier is added with a Trigger. This is applied if the client is a high risk. With no Sequence number, this calculation is performed on the Flat Amount that came first in the calculation order.

- A Rate is calculated based on the insured value. This is the first calculation of sequence 1.

- A Minimum amount is applied, in case the insured value does not meet minimum requirements. As the second calculation of sequence 1, the minimum is only compared to the result of the Rate calculation.

- The main Rate is now calculated based on the insured value. As the first calculation of sequence 2, this amount alone is passed to the next calculations.

- A Discount or Surcharge is added to the main rate, conditional on a Trigger. This adds a surcharge for certain types of insured property. This is the second calculation of sequence 2, but another Discount or Surcharge exists in this sequence, causing both to be combined.

- Another Discount or Surcharge is added with a Trigger. This provides a discount if this is a preferred client. Since we do not want to provide a discount on the Surcharge value, this is given the same Sequence number as the surcharge. If the triggers for the surcharge and the discount both evaluate as true, they are combined for a total value of 0.8 (20% discount), applied to the main Rate.

- The calculated totals of each sequence number, including the calculations without sequence numbers, are added together to produce the gross premium amount for this Premium Type.

Effective Date and Valid Until Date

The Effective Date and Valid Until Date fields can be used together or separately to control when the entry is applied. If the effective date of the transaction is before the effective date of the entry or after the valid until date of the entry, the calculation for this entry is not applied.